Certificado de Calidad

ISO 9001:2015 / ES-0395/2014-

-

Grupo Líder

En España

15 agosto, 2022

In this chapter, we begin examining the relationship among sales volume, fixed costs, variable costs, and profit in decision-making. We will discuss how to use the concepts of fixed and variable costs and their relationship to profit to determine the sales needed to break even or to reach a desired profit. You will also learn how to plan for changes itsdeductible in selling price or costs, whether a single product, multiple products, or services are involved. The Contribution Margin Ratio is a measure of profitability that indicates how much each sales dollar contributes to covering fixed costs and producing profits. It is calculated by dividing the contribution margin per unit by the selling price per unit.

- If you need to estimate how much of your business’s revenues will be available to cover the fixed expenses after dealing with the variable costs, this calculator is the perfect tool for you.

- Input Price per Unit and Variable Cost per Unit, and our calculator will help you estimate Contribution Margin.

- The Contribution Margin Calculator is a powerful tool that simplifies this critical calculation.

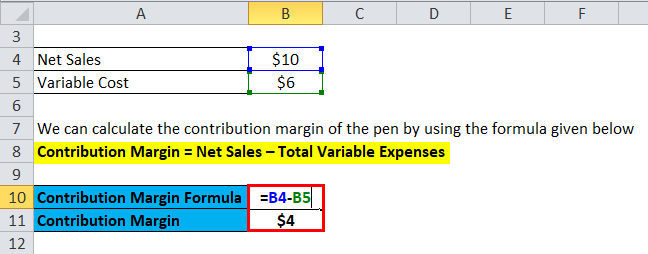

Formula and Calculation of Contribution Margin

Piece rate wages are paid based on the number of units produced; for example, if the piece rate wage is $4 per unit and a worker produces 10 units, then the total piece rate wage is $40. This example illustrates how understanding the contribution margin and contribution margin ratio can guide decisions related to pricing, product selection, and sales volume. For a small business owner, these insights are invaluable in achieving the break-even point and surpassing it towards profitability.

Unit Contribution Margin Explained

Fixed costs are costs that are incurred independent of how much is sold or produced. Buying items such as machinery is a typical example of a fixed cost, specifically a one-time fixed cost. Regardless of how much it is used and how many units are sold, its cost remains the same. However, these fixed costs become a smaller percentage of each unit’s cost as the number of units sold increases. It represents the incremental money generated for each product/unit sold after deducting the variable portion of the firm’s costs. For small businesses, mastering this aspect of financial analysis is a step towards sustained growth and success.

How Business Leaders Interpret Cost Behavior and Contribution Margin

If you need to estimate how much of your business’s revenues will be available to cover the fixed expenses after dealing with the variable costs, this calculator is the perfect tool for you. You can use it to learn how to calculate contribution margin, provided you know the selling price per unit, the variable cost per unit, and the number of units you produce. The calculator will not only calculate the margin itself but will also return the contribution margin ratio. Contribution margin income statement, the output of the variable costing is useful in making cost-volume-profit decisions. It is an important input in calculation of breakeven point, i.e. the sales level (in units and/or dollars) at which a company makes zero profit. Breakeven point (in units) equals total fixed costs divided by contribution margin per unit and breakeven point (in dollars) equals total fixed costs divided by contribution margin ratio.

What Is the Difference Between Contribution Margin and Profit Margin?

Get instant access to video lessons taught by experienced investment bankers. Learn financial statement modeling, DCF, M&A, LBO, Comps and Excel shortcuts. I understand this consent is not a condition to attend Florida Tech or to purchase any other goods or services. Risepoint maintains this website on behalf of Florida Institute of Technology. Florida Tech maintains responsibility for curriculum, teaching, admissions, tuition, financial aid, accreditation, and all other academic and instruction-related functions and decisions. For professionals looking to enhance their financial acumen and advance their careers, Florida Tech’s online MBA program offers comprehensive training in these critical areas.

How do you calculate the contribution margin?

The real power of understanding cost behavior comes into play when making critical business decisions. To set the right price for a new product, you must grasp how your costs will change as sales increase. When planning for future growth, cost behavior analysis helps predict how expenses will scale as your business expands. It even plays a vital role in break-even analysis, helping you pinpoint exactly when your venture will start turning a profit.

Generated profit is the amount of money that remains after all costs, both variable and fixed, have been paid. The relationship between Contribution Margin, sales, and profit is crucial in understanding this. Understanding the contribution margin of your products or services can guide critical decisions such as pricing, product mix, and cost management.

The contribution margin is given as a currency, while the ratio is presented as a percentage. Find out what a contribution margin is, why it is important, and how to calculate it. For instance, in Year 0, we use the following formula to arrive at a contribution margin of $60.00 per unit. One common misconception pertains to the difference between the CM and the gross margin (GM). If the contribution margin is too low, the current price point may need to be reconsidered.

© GRUPO EKONOMIKA , Creada por PSW Service.